From the Burj Khalifa to the China Zun, the following are the tallest buildings on the planet according to the Council on Vertical Urbanism, the Chicago-based non-profit organisation that has been setting the criteria for measuring their height since 1996

Design Economy 2026: Italy leads Europe in AI, sustainability and innovation

Text by

The European design sector is growing, driven by the digital and green transitions. Italy confirms its lead

Design, as we know, is a mirror of society – in particular, a litmus test of how technological innovation and industrial competitiveness are able to respond to the prevailing landscape and its challenges, not only market-related but, above all, social ones.

Presented by the Symbola Foundation, Deloitte Private, POLI.design and ADI Association for Industrial Design in collaboration with CUID, Interni Magazine, AIAP, AIPI, AlmaLaurea, the Guglielmo Tagliacarne Chamber of Commerce Research Centre, the ADI Design Museum and the Circolo del Design, under the patronage of the Ministry of Foreign Affairs and International Cooperation and the Ministry of Enterprise and Made in Italy, the Design Economy Report 2026 captures a sector undergoing profound transformation. An ecosystem which, whilst remaining closely linked to the historic Made in Italy supply chains, is rapidly evolving towards new production models, digital services, sustainability and artificial intelligence.

The economic weight of European design

The premise of the report is that European design is currently moving at two speeds - still poorly integrated into public agendas, yet increasingly recognised by businesses as a strategic lever for the green and digital transitions. Whilst the Nordic countries, the Netherlands and some European administrations are experimenting with design in public policies and services, in Southern Europe - including Italy - the link with the Made in Italy manufacturing sectors remains strong. Here too, however, the focus is gradually shifting from the product to the experience, digital services and new models of innovation.

In 2024, the European design sector comprised around 295,000 companies, generating a €31 billion turnover and employing over 356,000 people. These figures were on the rise: turnover increased by 3.2% compared to 2023 and by 23.8% over the three-year period, whilst employment grew by 4.8% year-on-year.

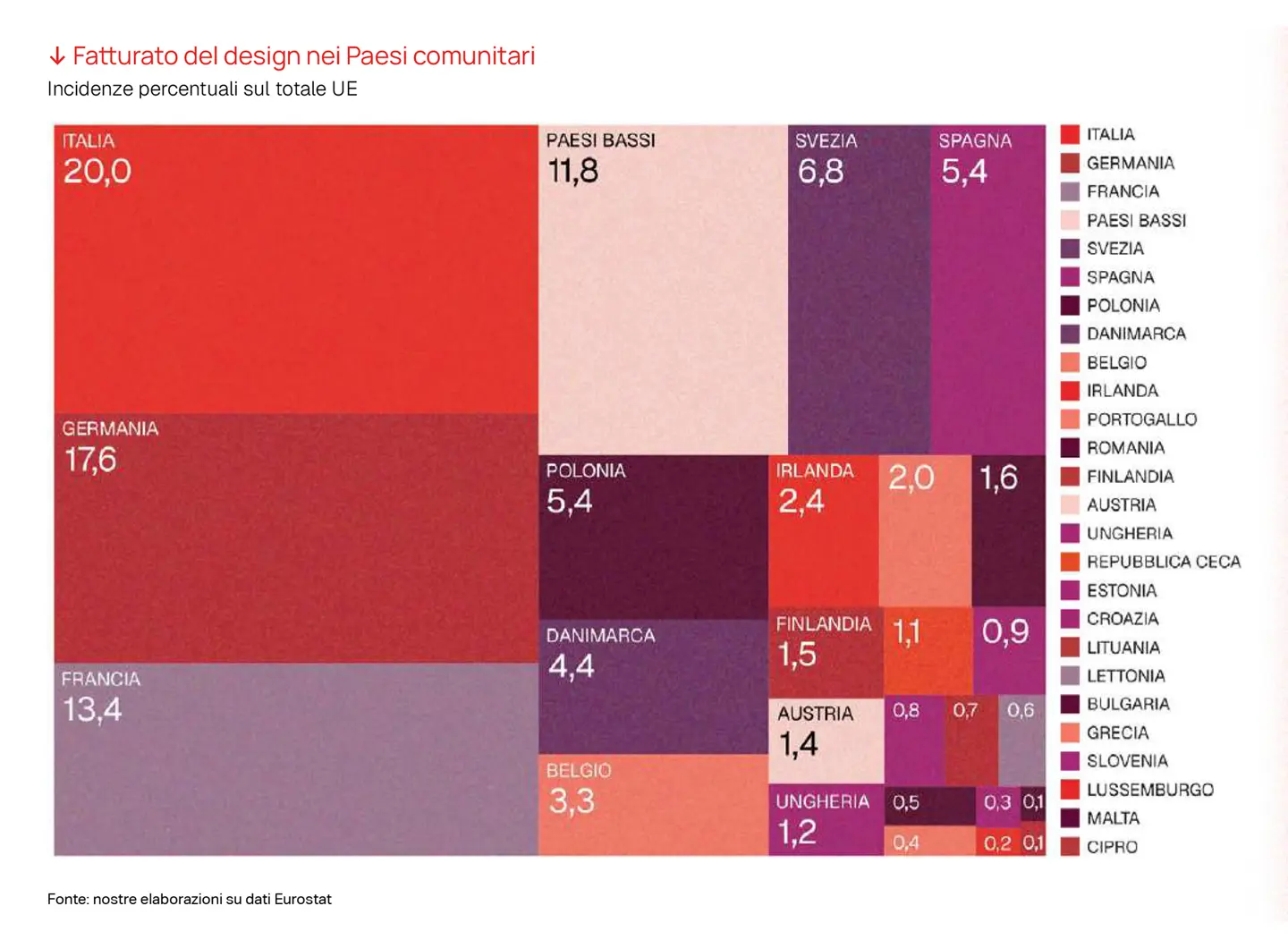

Italy confirmed its European leadership in terms of employee numbers: 54,000 design professionals and practitioners, accounting for 21.5% of the EU total. It was followed by France (14.9%) and Germany (14.0%). The Italian figure for employment growth was particularly significant: +9.8% in one year, almost double the European average. In terms of economic value, too, European design remained highly concentrated. Over half of the sector’s turnover was concentrated in three countries: Italy (20%), Germany (17.6%) and France (13.4%). Together with the Netherlands and Sweden, these accounted for nearly 70% of total European turnover.

At the same time, new dynamic regions were emerging: Latvia (+12.7%), Greece (+11.4%), Portugal (+9.7%) and Lithuania (+9.6%) demonstrated that design was becoming a driver of development even in economies previously considered marginal. The data on labour productivity is also interesting: the most efficient countries were Luxembourg, Denmark, Spain and Ireland, underscoring the correlation between average company size, organisational capacity and value generated per employee.

Italy: the European hub of design

With around 54,000 operators, including businesses, professionals and the self-employed, according to data collected by the report, Italy remained one of Europe’s leading design hubs and an international magnet for talent and creative centres. The sector generated around €4 billion in added value and employed over 76,000 people. The sector continued to grow - by 2024, employment rose by +9.8%, well above the average for the Italian economy.

Despite leading Europe in terms of workforce numbers, a productivity gap nevertheless remained compared to the EU average: €81,100 per employee versus €86,900 across Europe. According to the report, bridging this gap will require fostering the growth of businesses and strengthening the segments with the highest added value. Internationalisation also remained limited, with 89.5% of professionals working predominantly in the Italian market, whilst only 6.4% operated mainly within the European Union and 4.1% in non-EU markets.

Italian design remained strongly integrated into the manufacturing system, with demand also expanding into new areas such as healthcare, public administration, digital services, software, UX and service design. More and more companies were bringing design expertise in-house, turning design into a strategic function capable of influencing processes, services and user experience.

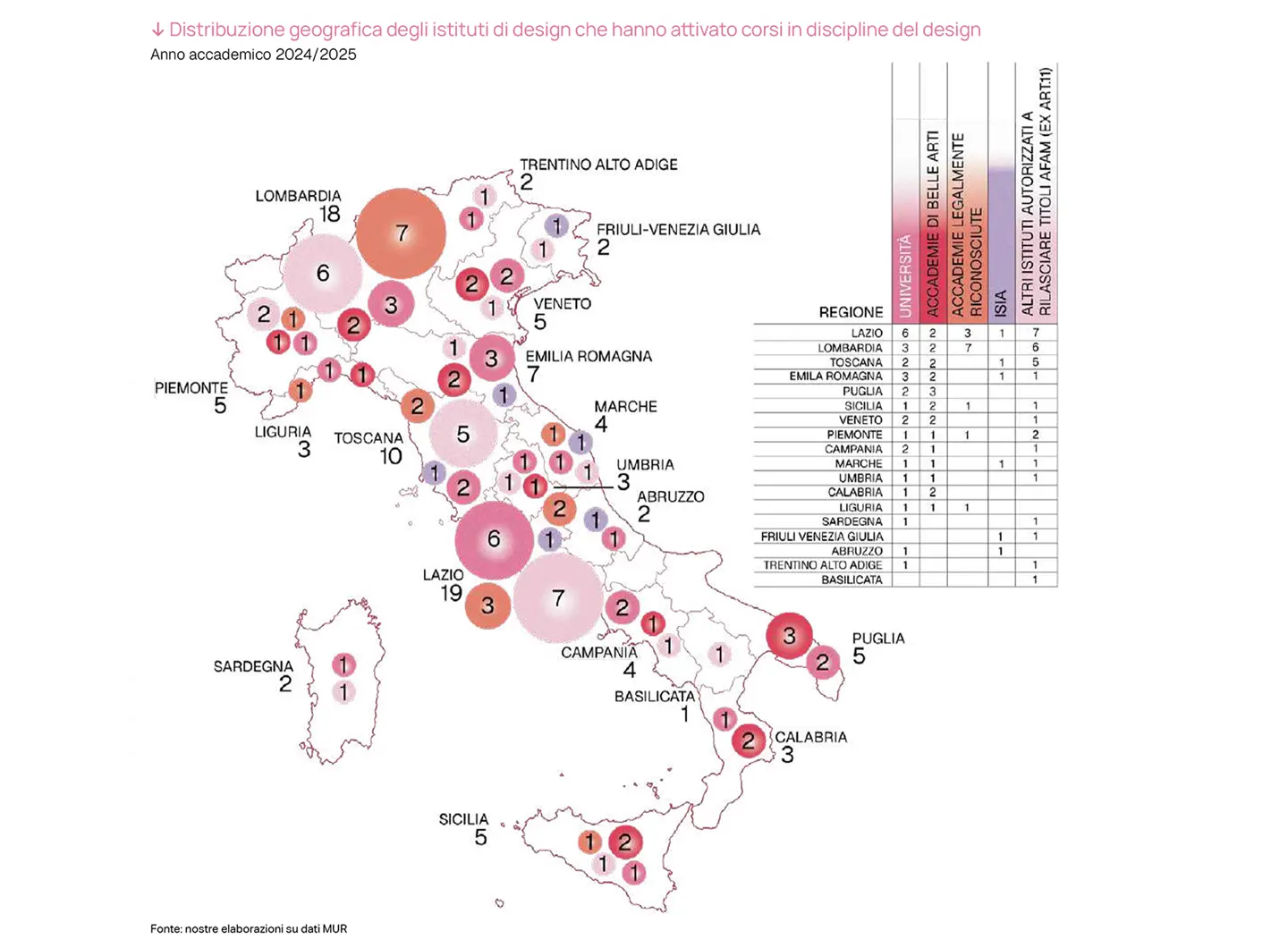

Italian design regions

Lombardy consolidated its position as the sector’s leading national driver: it alone generated 33.4% of added value and accounted for 28.7% of the workforce in Italian design. This lead reflected the density of the regional production system, the presence of advanced Made in Italy supply chains, and the integration of manufacturing, services, training and design culture. Milan represented the heart of this ecosystem. With over 7,300 active businesses, the province confirmed its leadership at national level and alone produced 19% of the design-generated wealth in Italy. It was also the main employment hub, accounting for 14.3% of the sector’s workforce nationwide.

Alongside Lombardy, Emilia-Romagna, Veneto and Piedmont remained key regions, accounting for 13.3%, 10.9% and 10.3% of national added value respectively. In terms of specialisation, however, manufacturing regions such as the Marche also made their presence felt, with design contributing 0.33% to the regional economy, thanks to the strength of the Made in Italy districts.

On an urban level, Milan retained its leadership, followed by Turin, Rome and Bologna, as well as by new dynamic areas, with Nuoro, Oristano, Ragusa, Catanzaro and Campobasso recording high growth rates, a sign of increasing vitality.

Employment and new professions

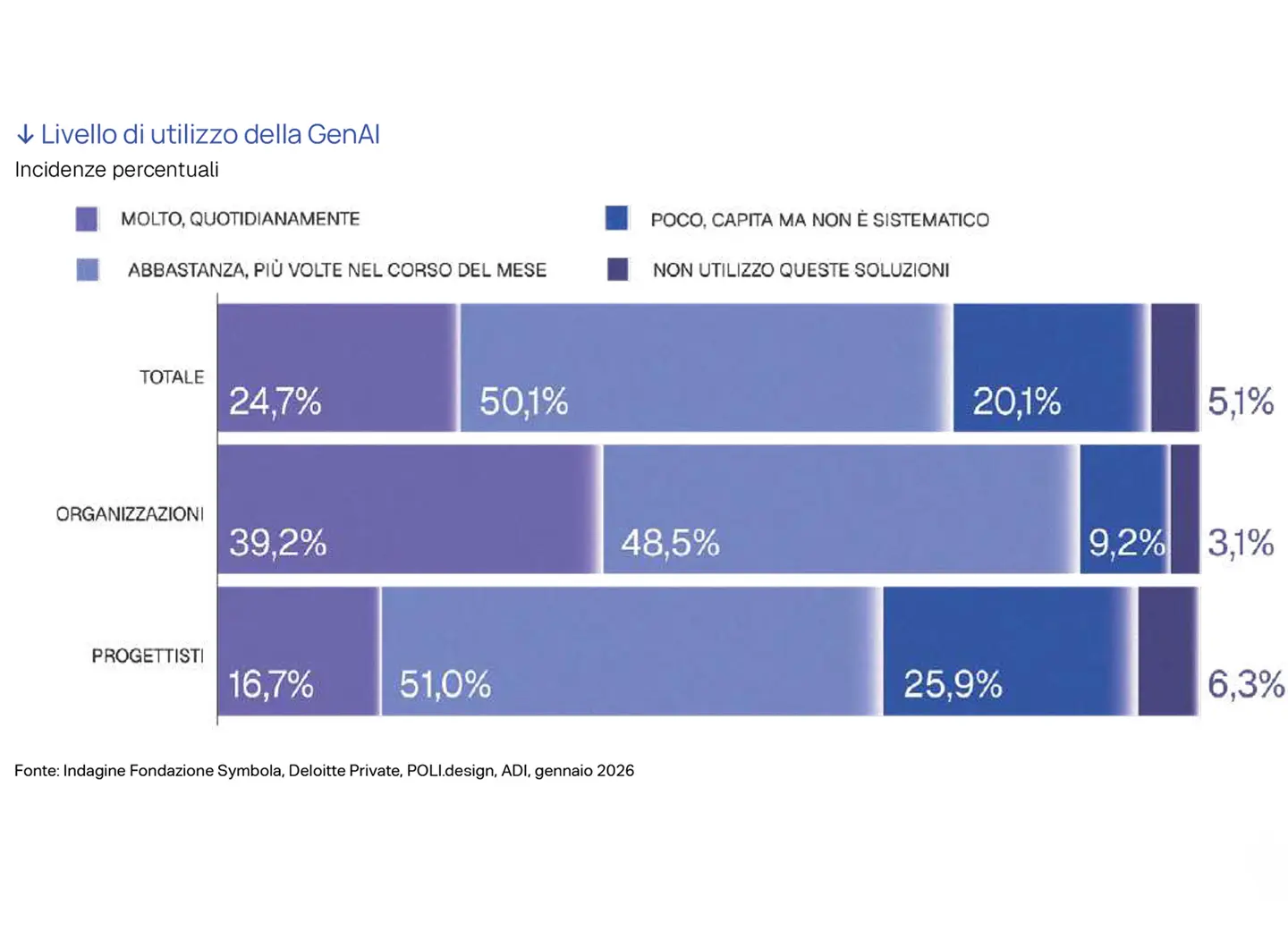

The Symbola report reminds us, with some specific focuses, that the world of design is undergoing a profound organisational transformation. Hybrid structures are emerging alongside traditional studios, and the sector appears less and less binary between salaried employment and freelance work, with multidisciplinary careers also on the rise. Equally, demand is growing for specialist skills related to sustainability and artificial intelligence. According to the survey conducted by Symbola, six out of ten designers have taken part in at least two training activities over the last year, and 90% of practitioners plan to invest in training in the near future.

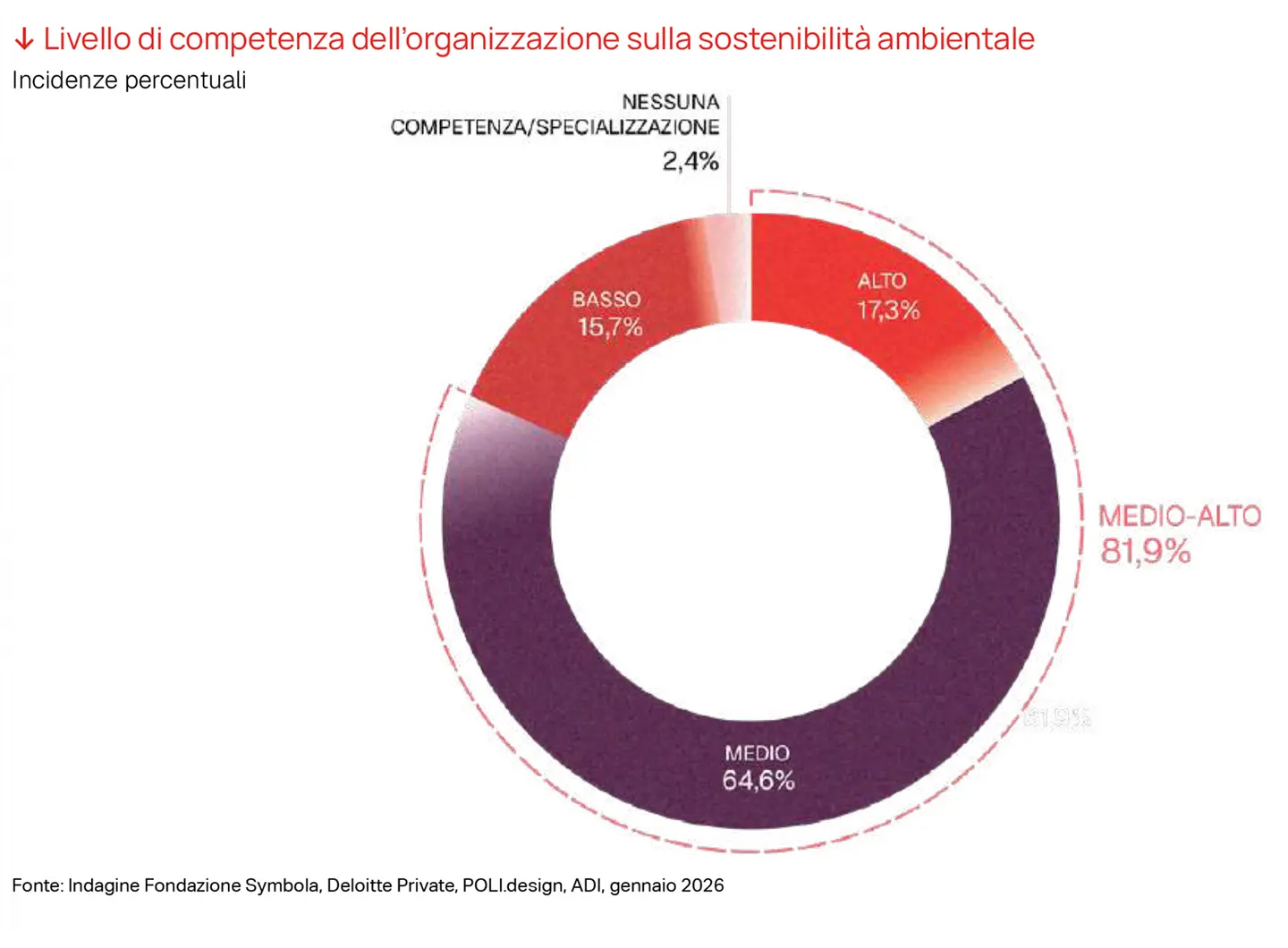

Right now, generative AI is the main driver of training for 66% of professionals. Just over half of professionals reported an average level of proficiency in generative technologies (indicating that skills were widespread but not yet fully established), whilst 35.4% of organisations reported a high level of proficiency. The adoption of GenAI tools mainly related to preliminary research, context analysis, product customisation, technical optimisation and feedback analysis. AI was therefore perceived primarily as an efficiency booster rather than a creative substitute. It was also a professional driver, and the roles considered most promising were those of Prompt Designers, Sustainability Designers, Material Designers and UI/UX Designers.

Ethical issues, however, remained central: almost 80% of respondents expressed concerns regarding copyright, content originality, privacy, process transparency and energy consumption. Equally, GenAI was seen as a useful tool for supporting sustainable practices: waste reduction, environmental impact simulations, circular design and product customisation.